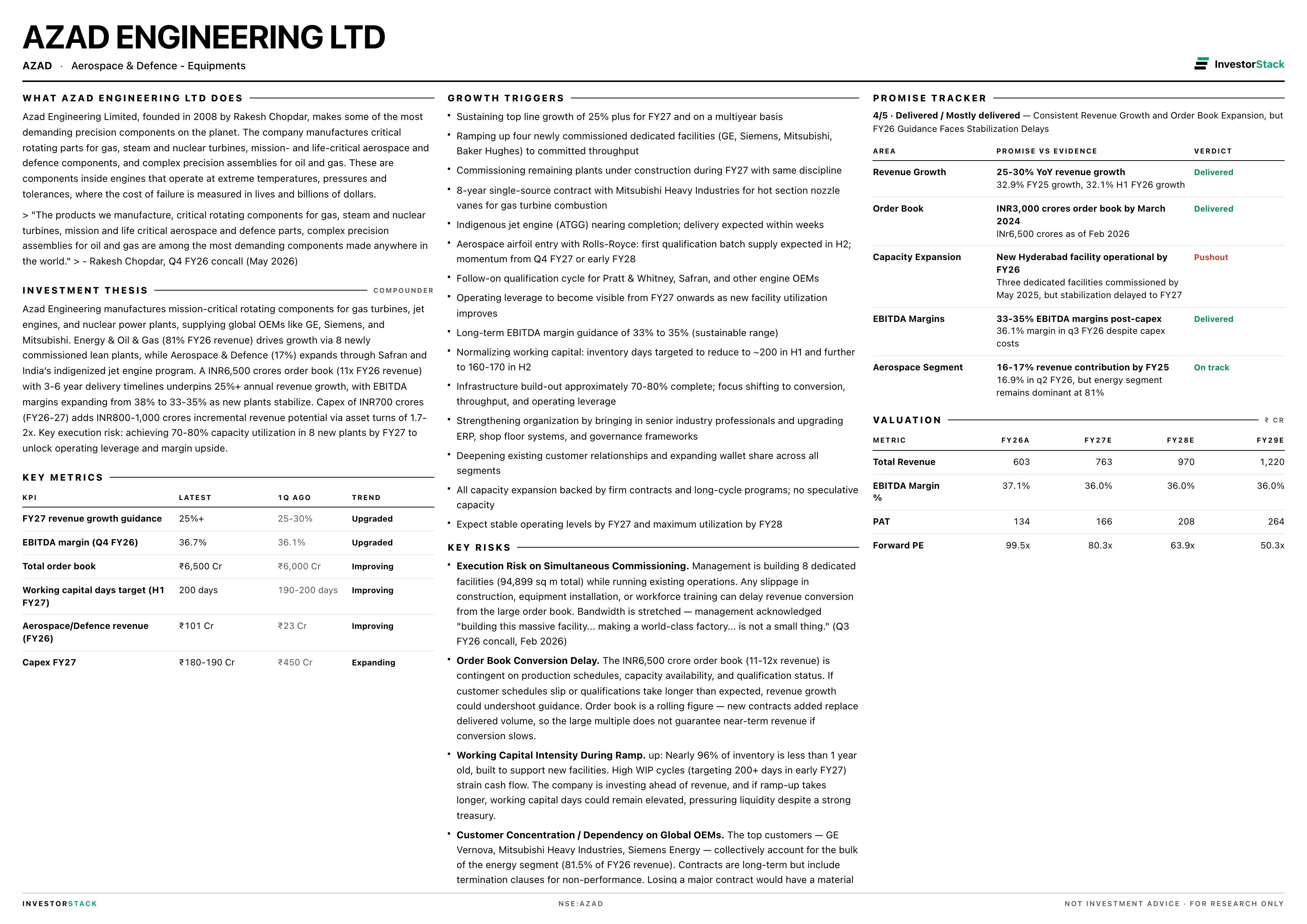

Azad Engineering

Riding the Turbine and Aerospace Cycle

Before we begin, Investorstack is now free to try. Research reports, valuation models, scanners, thematic baskets, industry reports, One pagers. All under one subscription.

Azad Engineering Limited was founded in 2008 by Mr. Rakesh Chopdar in Hyderabad, India. The company manufactures precision, mission-critical and zero-defect components for three industries: Aerospace and Defence, Power Generation, and Oil and Gas. Its parts sit inside industrial gas turbines, aircraft engines, nuclear power plants, missile systems and drilling rigs - applications where a single defect can cause catastrophic failure.

The company’s origin story is unusual in Indian manufacturing. Chopdar is a school dropout who began in his family’s small fasteners business generating roughly Rs1 million in revenue. His entry into precision manufacturing came when he reverse-engineered and replicated a precision component that had been rejected by an OEM, doing so without formal infrastructure or tooling. That single job led to initial job-shop orders, including from Saudi clients, which then scaled into airfoil manufacturing and a steady build-out of capability across forging, heat treatment, brazing, coatings and multi-axis machining. The company was formally incorporated as Azad Engineering in 2008 and has since grown to approximately 1,500 employees.

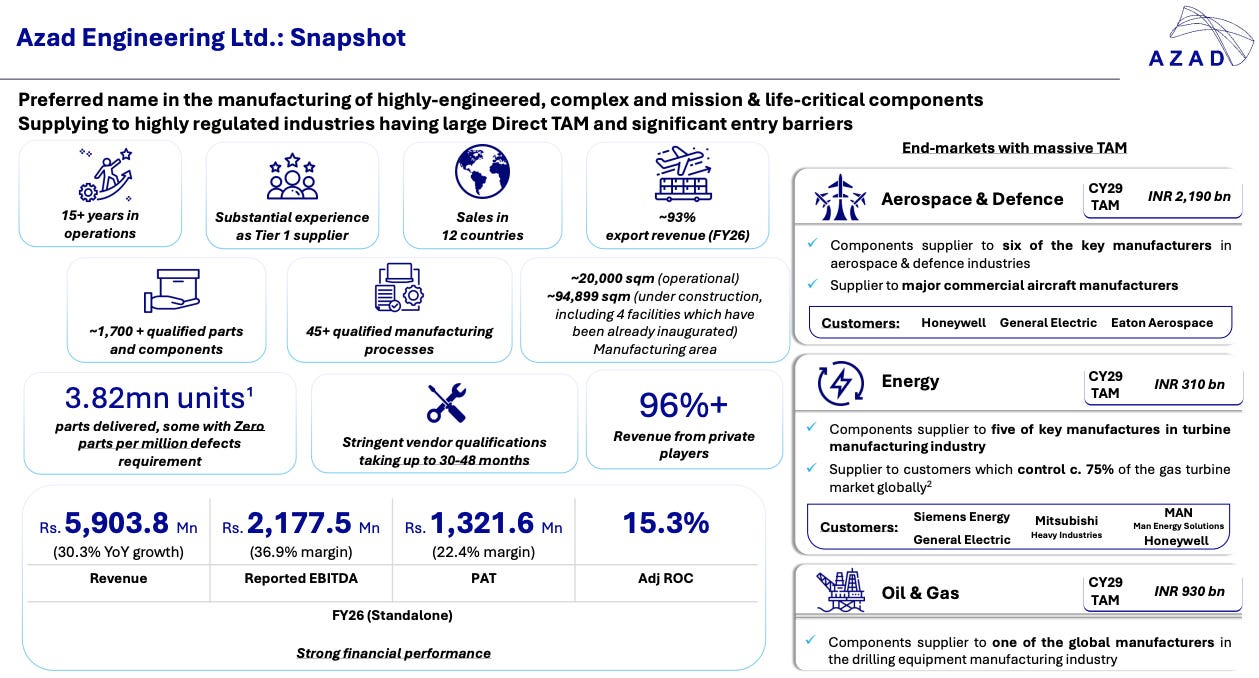

Azad went public on the NSE and BSE and raised approximately Rs7 billion through a Qualified Institutional Placement (QIP) to fund its Phase-1 capacity expansion. The company operates with a portfolio of 1,700+ qualified parts across 45+ specialised manufacturing processes. Its customer base includes GE Vernova, Mitsubishi Heavy Industries, Rolls-Royce, Honeywell Aerospace, Siemens Energy, Baker Hughes, Arabelle Solutions France, Bharat Heavy Electrical Limited (BHEL) and the Gas Turbine Research Establishment (GTRE) under DRDO.

The business is overwhelmingly export led. In FY25, the United States and Japan each accounted for approximately 38% of revenue, with the UAE at 9%, India at 13% and the remainder from Europe and other markets. Roughly 80% of revenue comes from exports.

The Energy segment has been growing at approximately 26% annually, while Aerospace and Defence grew 84% in FY25 off a smaller base, driven by completed OEM qualification cycles and execution ramp-up across multiple aircraft platforms.

The moat: the art of airfoil manufacturing

To understand why Azad is difficult to displace, you have to understand what an airfoil is and why making one is hard.

A gas turbine has three sections: compression, combustion and turbine. In the compression section, air is drawn in and compressed across multiple stages - typically 17 to 22+ stages in industrial gas turbines. Each stage requires blades (rotating) and vanes (stationary) with highly customised geometries, dimensions and tolerances. The compressor spins at approximately 15,000 RPM. The combustion section burns fuel at extreme temperatures. The turbine section extracts energy from the hot gas at approximately 4,000 RPM.

Azad currently specialises in the compression section, supplying high-precision airfoils and critical components. It is now strategically expanding into the combustion section, which involves higher heat tolerance and more complex manufacturing.

An airfoil cannot be produced by simply loading a CAD file into a CNC machine and pressing start. The outcome depends on integrated execution across five variables: choice of input material, choice of machinery, choice of fixture, choice of tools and choice of programming. Each variable interacts with the others. A different alloy behaves differently under the same cutting parameters. A different fixture changes vibration characteristics. A different tool path changes surface finish and dimensional accuracy. The "art" is the accumulated knowledge of how these variables interact, learned over years of producing thousands of parts across dozens of platforms.

This is why Azad describes its manufacturing as "man + machine + art" rather than a standardised production process. Two manufacturers with identical equipment will produce different quality levels because the tacit knowledge embedded in the workforce, the process recipes developed through trial and error, and the institutional memory of what works and what does not are not transferable.

The qualification cycle as a competitive moat

Every part Azad manufactures must go through a multi-year qualification process with each OEM. The process involves Request for Quotation (RFQ), First Article Inspection (FAI) validation, raw material and coating approvals, batch procurement requirements and consistent execution across price, lead time and quality parameters. Each component and each facility must undergo rigorous audits, testing and approvals.

Once a supplier is qualified, replacing them is extremely difficult. The OEM has invested years in auditing the supplier's processes, validating their parts and integrating them into their supply chain. Switching to a new supplier means restarting the entire qualification cycle, during which production of the affected turbine or engine platform could be delayed. This creates near-permanent vendor lock-in once approved.

OEM qualification typically begins with lower-stage compressor parts - simpler geometries with lower risk - and scales upward as the supplier demonstrates consistency. Azad has progressively qualified across more stages and more platforms over its 17-year history, accumulating 1,700+ qualified parts.

Build-to-print model with pricing protection

Azad operates on a build-to-print model. The OEM provides the design specifications, and Azad manufactures to those specifications. Most contracts follow fixed-price structures with a raw material volatility absorption threshold of approximately 4-5%. Beyond that threshold, cost increases are passed through to the OEM. This structure preserves margin stability across commodity price cycles and shifts raw material risk back to the customer.

The capability breadth advantage

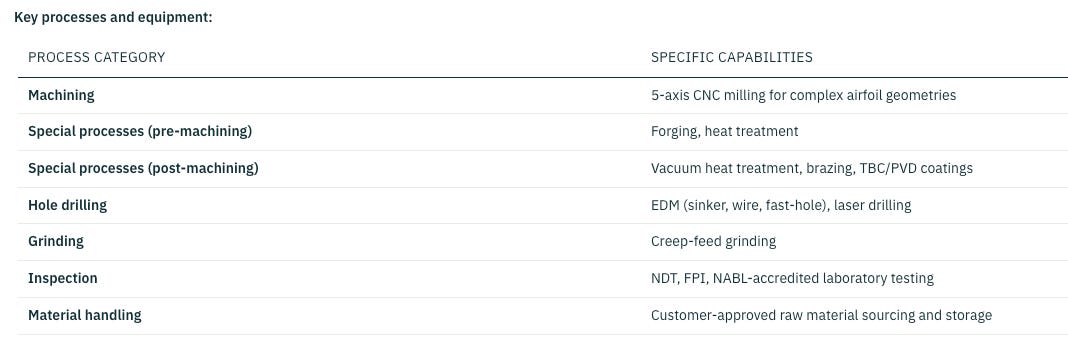

Azad performs an unusually broad set of manufacturing processes in-house. The 45+ specialised processes include 5-axis CNC milling, electrical discharge machining (EDM), creep-feed grinding, laser drilling, vacuum heat treatment, brazing, forging, thermal barrier coatings (TBC), physical vapour deposition (PVD) coatings, non-destructive testing (NDT) and fluorescent penetrant inspection (FPI). Among the six global Tier A precision machining peers benchmarked later in this report, Azad has the broadest capability set - spanning forging, 5-axis machining, EDM, laser, heat treatment, brazing and coatings, all under one roof.

This matters because it reduces dependency on external process suppliers, shortens lead times and gives Azad control over the entire quality chain. A competitor that must outsource heat treatment or coating to a third party introduces an additional point of failure and an additional lead time variable into a process where zero defects are required.

Manufacturing network

Existing Hyderabad facility

Azad’s original manufacturing complex in Hyderabad houses its core precision engineering operations. This facility can support approximately Rs4.5 billion in revenue at a blended asset turn of roughly 1.8x. Energy operations turn at approximately 1.7x, while Aerospace operations turn higher at approximately 2.5x due to lower capital intensity per part.

The facility produces the full range of Azad's product portfolio: compressor airfoils, turbine blades, aero engine components, APU parts, hydraulic and actuating system components, flight control parts, missile components and oil and gas drilling components. It houses 1,700+ qualified parts across 45+ specialised manufacturing processes.

Certifications:

NADCAP-approved equipment for special processes (the global aerospace standard for special process accreditation)

AS9100D certified (the international quality management standard for aviation, space and defence organisations)

NABL-accredited laboratory (National Accreditation Board for Testing and Calibration Laboratories)

NADCAP accreditation is critical. It is administered by the Performance Review Institute and is required by virtually every major aerospace OEM. Achieving NADCAP approval for a process means the facility has been audited and found compliant with stringent aerospace industry standards for that specific process. Azad maintains NADCAP approvals across multiple special processes, which is a narrower set of capabilities than most peers possess.

Phase-1 expansion: client-dedicated lean facilities

Azad is executing a Phase-1 capacity expansion at Hyderabad comprising nine new and planned client-dedicated lean manufacturing facilities. This expansion was funded through the approximately Rs7 billion QIP raised post-IPO.

The concept is that each major OEM customer gets a dedicated facility designed to their specifications and aligned with their processes. Three such facilities have already been inaugurated:

Mitsubishi Heavy Industries (MHI) dedicated facility - inaugurated March 12, 2025. Designed to MHI’s global specifications, this facility manufactures precision airfoils and turbine components for MHI’s industrial gas turbine platforms. The dedicated model means MHI’s processes, quality systems and logistics are embedded directly into the facility’s operations.

GE Vernova dedicated facility - inaugurated April 29, 2025. This facility manufactures gas and thermal turbine components for GE Vernova. It is designed to align with GE Vernova’s manufacturing processes and quality requirements, reducing turnaround times and improving operational efficiency.

Siemens Energy dedicated facility - inaugurated September 18, 2025. Dedicated to manufacturing precision turbine components for Siemens Energy’s gas and steam turbine platforms.

The Phase-1 expansion raises Azad’s total potential revenue capacity from approximately Rs4.5 billion to approximately Rs20 billion - a roughly 10x increase. With each new facility estimated to support approximately Rs2 billion in revenue, the nine facilities add approximately Rs18 billion of potential revenue visibility on top of the existing Rs4.5 billion base. Projected revenue with existing capex plans reaches approximately Rs22.5 billion.

The dedicated facility model serves multiple purposes. It deepens OEM integration by making Azad’s operations an extension of the customer’s own manufacturing system. It improves turnaround times by eliminating the need to switch between different customers’ processes on shared equipment. And it creates a physical manifestation of the customer relationship that makes switching suppliers even more difficult - the OEM has invested time and capital in setting up a facility to their specifications, and walking away from it would mean restarting that investment elsewhere.

Phase-2 capacity expansion

Azad has announced plans for a Phase-2 capacity expansion beyond the current Phase-1 build-out. This expansion is intended to support execution of the growing order pipeline and further enhance OEM integration. Specific details on capacity, timeline and investment for Phase-2 have not yet been disclosed, but the company has indicated that the Phase-1 facilities alone may not be sufficient to meet demand from existing and prospective customers.

Strategic acquisitions

Azad has made small strategic acquisitions, including Azad VTC, to strengthen vertical integration and execution capability. These acquisitions are targeted at adding specific process capabilities or customer relationships rather than scaling revenue through inorganic growth.

Management team

Mr. Rakesh Chopdar - Founder and Promoter

Rakesh Chopdar founded Azad Engineering in 2008. He is a school dropout who began his career in his family’s small fasteners business, which generated approximately Rs1 million in revenue. His entry into precision manufacturing came when he replicated a rejected precision component without formal infrastructure or tooling - an achievement that demonstrated both technical aptitude and an ability to solve problems without conventional resources.

Initial job-shop orders, including from Saudi clients, scaled into airfoil manufacturing. Chopdar then built out capability methodically, adding processes one at a time: machining first, then forging, then heat treatment, then brazing, then coatings. Each addition was driven by customer requirements and qualification opportunities rather than speculative capacity building.

Chopdar’s background means the company’s DNA is execution-first rather than strategy-first. The capability set was built from the shop floor upward, with each new process added only when there was a customer pulling for it. This is reflected in the company’s build-to-print model, where the focus is on manufacturing excellence rather than product design or IP creation.

The company has expanded its leadership team in recent periods, though specific names and backgrounds beyond the founder have not been detailed in available disclosures. The expanded team is expected to support the transition from a founder-driven organisation to a professionally managed one as the company scales from approximately Rs4.5 billion to Rs20 billion in revenue capacity.

Certifications and quality systems

Azad’s ability to serve global aerospace and energy OEMs depends on maintaining a stack of certifications and accreditations that are independently audited and renewed periodically.

AS9100D is the international quality management standard for aviation, space and defence organisations. It encompasses ISO 9001 requirements plus additional aerospace-specific requirements for configuration management, risk management, counterfeit parts prevention and special processes. Azad has been AS9100D certified, meaning its quality management system meets the standard required by every major aerospace OEM.

NADCAP (National Aerospace and Defense Contractors Accreditation Program) is administered by the Performance Review Institute. Unlike AS9100D, which certifies a quality management system, NADCAP certifies specific special processes - heat treatment, coatings, NDT, welding, brazing, chemical processing and others. Each process requires a separate audit and accreditation. Azad maintains NADCAP approvals across multiple special processes, which places it in a narrow group of global suppliers qualified to perform these processes for aerospace OEMs.

NABL (National Accreditation Board for Testing and Calibration Laboratories) accreditation means Azad’s in-house laboratory meets national standards for testing and calibration. This allows Azad to perform material verification, dimensional inspection and non-destructive testing in-house rather than relying on external laboratories, reducing lead times and maintaining quality control over the entire process chain.

The certification stack creates a regulatory and quality barrier that compounds with the qualification cycle. A new entrant must not only build the physical capability to manufacture precision parts but also invest years in achieving and maintaining these accreditations before they can even begin the OEM qualification process.

Product portfolio

Azad’s product portfolio spans three end markets with 1,700+ qualified parts. The products below are organised by segment and represent the core manufacturing programmes that define the company’s revenue and growth trajectory.

Energy products

The Energy segment contributed 79% of FY25 revenue. Products in this segment serve industrial gas turbines, steam turbines and nuclear power plants, with applications across natural gas, hydrogen-ready, thermal and nuclear fuel types.

Compressor airfoils (3D rotating and stationary)

What it is: Precision-machined 3D airfoils and blades for the compressor section of industrial gas turbines. These are the rotating and stationary blades that compress incoming air across multiple stages before it enters the combustion chamber.

Product type: Precision-machined turbine component, manufactured via 5-axis CNC milling from nickel-based superalloys, with in-house forging, heat treatment, brazing and coatings.

The advantage: A multi-stage compressor in an industrial gas turbine has 17 to 22+ stages, each requiring highly customised blades with different dimensions, tolerances and geometries. There is no standardised production pathway for these parts. The blade for stage 3 is different from the blade for stage 12, which is different again from stage 20. Each blade must be manufactured to tolerances measured in microns, with zero defects, because a failure at 15,000 RPM inside a turbine running continuously for months is catastrophic.

The advantage Azad brings is integrated execution across the entire manufacturing chain. Unlike competitors who may outsource forging, heat treatment or coatings, Azad performs all of these in-house. This means the company controls every variable that affects part quality: the input material selection, the forging parameters, the machining tool paths, the heat treatment cycles, the coating application and the final inspection. When a customer needs a new stage qualified, Azad can iterate across all these processes internally rather than coordinating across multiple external suppliers.

OEM qualification typically begins with lower-stage parts, where geometries are simpler and risk is lower. As the supplier demonstrates consistency over multiple production runs, the OEM qualifies them for higher stages with more complex geometries and tighter tolerances. Azad has progressively qualified across more stages and more turbine platforms over its history, and continues to expand its qualified stage coverage.

Addressable market: The airfoil-specific segment (by blade shape) was approximately USD 5 billion in 2024 and is expected to reach USD 9 billion by 2035, growing at roughly 6% annually. The nickel-based superalloy segment alone was valued at approximately USD 6 billion in 2024.

Launch timeline: Already commercialised. Ongoing qualification expansion across additional compressor stages and turbine platforms.

Clinical status: Commercialised with 1,700+ qualified parts across the portfolio.

Commercialization partners: GE Vernova, Mitsubishi Heavy Industries, Siemens Energy, Arabelle Solutions France.

Turbine blades (precision machined)

What it is: Precision-machined turbine blades for the hot section of industrial gas turbines, where extracted energy from combusted gas drives the turbine rotor.

Product type: Precision-machined turbine component manufactured from nickel-based superalloys, requiring zero-defect execution and full-process traceability.

The advantage: Turbine blades operate in the most extreme environment inside a gas turbine. They sit directly in the path of hot combustion gases, requiring materials and manufacturing processes that can withstand sustained high temperatures and centrifugal forces. The blades are manufactured from nickel-based superalloys, which retain their mechanical properties at temperatures that would destroy conventional materials.

The manufacturing challenge is that these superalloys are difficult to machine. They are hard, gummy and work-harden during cutting, which means the cutting tool encounters progressively harder material as it cuts. This requires specialised tooling, optimised cutting parameters and careful process control to achieve the required tolerances without inducing residual stresses or surface defects. Azad’s in-house capability across machining, heat treatment and coatings means it can control the entire process chain - from raw material through to finished blade - without handing off to external suppliers who might introduce variability.

Azad supplies these blades to the major global gas turbine OEMs. The turbine blade sub-segment was approximately USD 4-5 billion in 2024 and is expected to reach USD 7-8 billion by 2035.

Addressable market: Turbine blade sub-segment of approximately USD 4-5 billion in 2024, expected to reach USD 7-8 billion by 2035, growing at approximately 6% annually.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: GE Vernova, Mitsubishi Heavy Industries, Siemens Energy, Rolls-Royce.

Combustion component assemblies

What it is: Component assemblies for the combustion section of industrial gas turbines, where fuel is mixed with compressed air and ignited to produce high-pressure, high-velocity gas that drives the turbine.

Product type: Higher-value precision-machined turbine component, representing a strategic expansion beyond Azad’s core compressor airfoil business.

The advantage: The combustion section operates at higher temperatures than the compression section, requiring components with greater heat tolerance and more complex geometries. Moving from compressor airfoils into combustion components is a natural but technically demanding progression up the turbine value chain.

The advantage of this expansion is wallet share. A turbine has both a compression section and a combustion section. If Azad supplies only compressor airfoils, it captures a fraction of the total component spend per turbine platform. By qualifying for combustion components as well, Azad can double or triple its revenue per turbine platform from the same customer, without needing to win a new customer. The customer already knows Azad’s quality systems, has audited its facilities and has integrated it into their supply chain. Adding new part families to an existing qualified supplier is far easier for the OEM than qualifying a new supplier.

Combustion components also require higher heat tolerance, which means different materials, different coating systems and different process parameters. This raises the technical barrier and means fewer competitors are qualified to manufacture them. Management has highlighted a roadmap to expand into combustion components with higher heat tolerance, implying deeper turbine integration over time.

Addressable market: Part of the broader energy turbine components market of approximately Rs280 billion in 2022, within a total energy TAM of Rs1,280 billion expected to reach Rs1,810 billion by 2027.

Launch timeline: Strategic expansion underway. Qualification in progress with early commercialisation.

Clinical status: Qualification phase and early commercialisation.

Commercialization partners: GE Vernova, Siemens Energy.

Aerospace and Defence products

The Aerospace and Defence segment contributed 17.9% of FY25 revenue and grew 84% year-on-year. Products in this segment serve commercial aviation, defence aircraft, spacecraft and missile systems.

Aero engine airfoils, blades and components

What it is: Precision-machined airfoils, blades and other critical components for aircraft jet engines, including components for the compressor and turbine sections of turbofan and turbojet engines.

Product type: Precision-machined aero engine component, manufactured under NADCAP-approved processes with zero-defect requirements.

The advantage: Aircraft engine components are mission-critical and life-critical. A failure in flight is not recoverable. This means every part must meet zero-defect standards, with full traceability from raw material through to finished component. The qualification cycle for aero engine parts is typically longer than for industrial gas turbine parts because the consequences of failure are more severe and the regulatory oversight (FAA, EASA) is more stringent.

Azad supplies components for major aircraft platforms including the Boeing 737, 737 Max, 747, 777, 777X, Airbus A320, A350, A355, A350 XWB and Gulfstream G550. Each platform has its own engine variant (CFM LEAP, GE9X, Rolls-Royce Trent, Pratt and Whitney GTF, etc.), and each engine variant requires its own set of qualified parts. The breadth of platforms Azad serves reflects years of incremental qualification wins.

The advantage is that once qualified on a platform, Azad becomes embedded in that engine programme’s supply chain for the entire production life of the engine, which can span 20-30 years. New engine programmes are launched infrequently, and once a supplier is locked in, the switching cost for the OEM is enormous - not just in re-qualification time and cost, but in the risk of disrupting production of an engine that may have a 14-year backlog.

Azad’s FY25 revenue of approximately USD 65 million represents less than 0.5% of the global aircraft engine blade market. Even within the narrower precision-machined airfoil niche estimated at USD 3-4 billion globally, Azad’s share is only 1.5-2%. This underscores the runway for growth as the company scales production and adds new OEM qualifications.

Addressable market: Aircraft engine blade market (all types) of approximately USD 13.5-15.6 billion in 2024, expected to reach USD 21-28 billion by 2032-2035, growing at 5.5-6.9% annually. Azad’s current share is less than 0.5%.

Launch timeline: Already commercialised. Expanding across new platforms and engine variants.

Clinical status: Commercialised with multiple OEM qualifications.

Commercialization partners: Rolls-Royce, Honeywell Aerospace, GE Aerospace.

Auxiliary Power Unit (APU) components

What it is: Precision-machined components for Auxiliary Power Units, which are small gas turbine engines typically located in the tail of an aircraft that provide power for ground operations and main engine starting.

Product type: Precision-machined aero component, manufactured under NADCAP-approved processes with zero-defect requirements.

The advantage: APUs are essential for aircraft operations. They provide electrical power and compressed air when the main engines are not running, and they start the main engines. Without a functioning APU, an aircraft cannot operate. This makes APU reliability critical and APU component manufacturing a zero-defect environment.

The demand driver for APU components is particularly strong right now. Maintenance turnaround times for APUs have increased sharply as the global fleet ages and parts shortages persist. Airlines are keeping aircraft in service longer - the average aircraft age climbed to 13.4 years in 2024 from 12.5 years in 2023 - and older APUs require more frequent servicing and replacement parts. This creates a sustained aftermarket demand stream that is less cyclical than new aircraft production.

Azad manufactures APU components under NADCAP-approved processes for Honeywell Aerospace, one of the dominant APU manufacturers globally. The qualification cycle for APU components is similar to that for engine components - multi-year, with rigorous audits and testing - meaning once qualified, Azad’s position as a supplier is difficult to displace.

Addressable market: Part of the global aerospace components TAM of approximately Rs990 billion in 2022, growing to approximately Rs1,530 billion by 2027 at roughly 9% annually.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partner: Honeywell Aerospace ISC, USA.

Hydraulic system components

What it is: Precision-machined components for aircraft hydraulic systems, which use pressurised fluid to transmit force for operating landing gear, flaps, brakes, spoilers and other flight surfaces.

Product type: Precision-machined aero component, manufactured to zero-defect standards with NADCAP-approved special processes.

The advantage: Hydraulic systems are the muscles of an aircraft. When a pilot moves the controls, hydraulic actuators convert that input into physical movement of control surfaces. A failure in the hydraulic system means the pilot cannot control the aircraft. Every component in the hydraulic circuit - valves, actuators, manifolds, fittings - must therefore meet zero-defect standards.

The manufacturing challenge is that hydraulic components often require tight internal geometries and surface finishes that must withstand high-pressure fluid without leakage or wear. The materials must resist corrosion and fatigue over thousands of flight cycles. Manufacturing these parts requires precision machining combined with specialised surface treatments and coatings, all of which Azad performs in-house.

The lengthy OEM qualification cycle for hydraulic components creates high entry barriers and customer stickiness. Once an OEM has qualified Azad to produce a hydraulic component, the cost and risk of re-qualifying a different supplier acts as a powerful retention mechanism. The component may be small, but the consequences of failure are severe, so OEMs are extremely conservative about changing suppliers.

Addressable market: Part of the global aerospace components TAM of approximately Rs990 billion in 2022, growing to approximately Rs1,530 billion by 2027.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: Multiple global OEMs.

Actuating system components

What it is: Precision-machined components for aircraft actuating systems, which convert hydraulic or electric power into mechanical motion to operate flight control surfaces, landing gear doors, thrust reversers and other moving parts.

Product type: Precision-machined aero component, manufactured under stringent multi-year qualification cycles.

The advantage: Actuating system components sit at the intersection of hydraulic power and mechanical motion. They must convert fluid pressure into precise, repeatable movement - extending landing gear at exactly the right speed, deploying flaps at exactly the right angle, deploying thrust reversers at exactly the right moment. The precision required is extraordinary, and the failure mode is severe.

What makes this product category defensible is the qualification cycle. Each actuating component must undergo rigorous audits, testing and approvals before it can be installed on an aircraft. The qualification process verifies not just the part itself but the entire manufacturing chain - the raw material, the machining process, the surface treatment, the inspection methodology and the documentation trail. Once an OEM has invested years in qualifying a supplier for an actuating component, replacing that supplier means restarting the entire process, during which the affected aircraft programme could face delays.

This is why vendor replacement is extremely challenging once qualified. The OEM has effectively bet their programme on the supplier’s ability to deliver zero-defect parts consistently, and they have verified that bet through years of auditing and testing. Walking away from that investment is not a decision any programme manager makes lightly.

Addressable market: Part of the global aerospace components TAM of approximately Rs990 billion in 2022, growing to approximately Rs1,530 billion by 2027.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: Multiple global OEMs.

Flight control components

What it is: Precision-machined components for aircraft flight control systems, including parts for the primary flight controls (ailerons, elevators, rudder) and secondary flight controls (flaps, slats, spoilers, trim tabs).

Product type: Life-critical precision-machined aero component with zero-defect requirements.

The advantage: Flight control components are life-critical. If a flight control fails, the pilot cannot maintain control of the aircraft. There is no redundancy for the component itself - while aircraft have redundant flight control systems, each individual component within those systems must function perfectly every time.

This creates the highest possible quality bar. Precision, reliability and process expertise are non-negotiable. The manufacturing tolerances are among the tightest in aerospace, and the inspection requirements are among the most rigorous. Any defect - a surface imperfection, a dimensional deviation, a material anomaly - could propagate into a failure under the cyclic loading that flight control components experience over thousands of flight cycles.

The qualification cycle for flight control components is among the longest in aerospace. The near-permanent vendor lock-in once approved is a direct consequence of the severity of failure. An OEM that has qualified a supplier for flight control components has essentially verified that supplier’s entire manufacturing process chain to the highest standard in the industry. Repeating that verification with a new supplier would take years and introduce unacceptable risk.

Addressable market: Part of the global aerospace components TAM of approximately Rs990 billion in 2022, growing to approximately Rs1,530 billion by 2027.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: Multiple global OEMs.

Fuel and inerting section components

What it is: Precision-machined components for aircraft fuel systems and inerting systems. Fuel systems manage the storage, distribution and delivery of jet fuel to engines. Inerting systems reduce the flammability of fuel tank vapours by replacing oxygen with nitrogen-enriched air, preventing explosions.

Product type: Precision-machined aero component, manufactured to zero-defect standards with NADCAP-approved special processes.

The advantage: Fuel system components must handle jet fuel at varying pressures and temperatures while maintaining perfect sealing. A fuel leak in an aircraft is a fire hazard. The materials must resist chemical degradation from prolonged fuel exposure, and the manufacturing tolerances must ensure leak-free assembly.

Inerting system components are a more recent addition to aircraft design, mandated after the TWA Flight 800 explosion in 1996 demonstrated the danger of fuel tank vapour ignition. These systems require precision components that can handle nitrogen-enriched air at specified pressures and flow rates. Because the technology is relatively new, the supplier base is narrower and the qualification opportunities are growing as more aircraft incorporate inerting systems.

Azad manufactures these components under NADCAP-approved special processes, ensuring that the coatings, heat treatments and surface finishes meet aerospace standards for fuel system applications. The combination of chemical resistance requirements, leak-free tolerances and NADCAP process accreditation creates a qualification barrier that limits the competitive field.

Addressable market: Part of the global aerospace components TAM of approximately Rs990 billion in 2022, growing to approximately Rs1,530 billion by 2027.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: Multiple global OEMs, including commercial and defence aircraft and spacecraft manufacturers.

Missile components

What it is: Various critical precision-machined components for missile systems, serving defence applications where component failure is not an option.

Product type: Precision-machined defence component, manufactured with zero-defect requirements.

The advantage: Missile components must function reliably after being subjected to extreme conditions - high-G launch accelerations, thermal extremes, vibration and shock. Unlike aircraft components that can be inspected and maintained between flights, missile components must work perfectly the one time they are called upon, often after years in storage.

The manufacturing requirements combine the precision of aerospace machining with additional challenges around long-term storage stability and one-time-use reliability. Materials must resist corrosion over years of storage, and the manufacturing process must produce parts that will function identically whether they are used immediately or after a decade in a silo.

Azad’s entry into missile component manufacturing leverages its existing precision machining and special process capabilities while adding defence-specific qualifications. The defence qualification process is separate from commercial aerospace qualifications and involves additional security clearances and compliance requirements. This further narrows the competitive field and creates additional barriers to entry beyond those already present in commercial aerospace.

Addressable market: Part of India’s defence indigenisation opportunity. India’s defence procurement budget and push for self-reliance in defence manufacturing creates a growing domestic market for qualified precision component suppliers.

Launch timeline: Already commercialised.

Clinical status: Commercialised.

Commercialization partners: Defence OEMs and DRDO.

Oil and Gas products

The Oil and Gas segment contributed approximately 3% of FY25 revenue. Products serve the exploration and production phase of the oil and gas value chain.

Drill bits and drilling equipment components

What it is: Precision-machined components for drilling rigs, including drill bits and other critical parts used in drilling equipment for oil and gas exploration and production.

Product type: Precision-machined oilfield component, manufactured from specialised alloys for high-temperature and high-pressure environments.

The advantage: Drilling rig components operate in some of the harshest conditions in industrial engineering. Downhole temperatures can exceed 200 degrees Celsius, pressures can reach 20,000 PSI, and the components must withstand abrasive rock formations, corrosive fluids and extreme mechanical loads. A drill bit failure at depth means pulling the entire drill string - a operation that can cost hundreds of thousands of dollars per day in rig time.

The components are manufactured from specialised alloys capable of maintaining their mechanical properties under these conditions. The machining challenges include working with hard, wear-resistant materials that are difficult to cut, achieving geometries that optimise drilling efficiency, and applying surface treatments that extend component life in abrasive environments.

High entry barriers exist due to stringent qualification requirements and long certification cycles. Oil and gas OEMs like Baker Hughes require suppliers to demonstrate consistent quality over extended periods before qualifying them for critical drilling components. Once qualified, the supplier benefits from the same vendor lock-in dynamics seen in aerospace and energy - the cost and risk of switching suppliers for downhole components is high enough that OEMs prefer to stay with proven suppliers.

Addressable market: Part of the global oil and gas equipment market. Azad is expanding its portfolio across upstream and midstream applications, growing beyond its initial drill bit component range.

Launch timeline: Already commercialised. Portfolio expanding.

Clinical status: Commercialised.

Commercialization partner: Baker Hughes (Nuovo Pignone srl).

Defence and propulsion systems

This category represents Azad’s strategic entry into complete propulsion system manufacturing, moving beyond component supply toward full engine assembly and integration.

Advanced Turbo Gas Generator Engine (GTRE)

What it is: A completely assembled Advanced Turbo Gas Generator Engine, manufactured under a single-source contract from the Gas Turbine Research Establishment (GTRE), a pioneering R&D organisation under DRDO and the Ministry of Defence, Government of India.

Product type: Complete propulsion system manufacturing - encompassing end-to-end manufacturing, assembly and integration of a fully assembled turbo engine.

The advantage: This is a fundamental shift in Azad’s business model. Until now, the company has been a component supplier - manufacturing individual parts that OEMs integrate into larger systems. The GTRE contract elevates Azad to the role of a complete engine manufacturer, responsible for manufacturing, assembling and integrating a fully functional turbo gas generator engine.

The engine is a critical development for India’s defence propulsion capabilities. It will be utilised in various defence applications, and Azad’s role as the single-source Industry Partner means no other company is authorised to manufacture this engine. This creates a monopoly position for the specific engine programme.

The strategic significance extends beyond the immediate contract. Manufacturing a complete turbo engine requires capabilities that Azad has been building incrementally - machining, assembly, testing, integration - but at a system level rather than a component level. If Azad successfully delivers this engine, it positions itself for future indigenous engine programmes, including potential serialisation of the Kaveri engine programme and other defence propulsion systems.

The near-term revenue from this contract is limited - estimated at Rs50-150 million - but the long-term optionality is significant. If indigenous engine serialisation proceeds, the revenue opportunity could scale to Rs300-1,000 million or more. The contract also provides Azad with defence aero-engine qualification experience that is extremely difficult to acquire through commercial channels, potentially opening doors to additional defence propulsion programmes.

Addressable market: Limited near-term revenue (Rs50-150 million). Long-term optionality of Rs300-1,000 million or more, contingent upon indigenous engine serialisation and the trajectory of India’s defence propulsion indigenisation programme.

Launch timeline: First batch of fully integrated turbo engines expected to be delivered by early 2026.

Clinical status: In development. First deliveries expected early 2026.

Commercialization partner: GTRE (Gas Turbine Research Establishment, DRDO, Ministry of Defence, Government of India). Azad is the single-source Industry Partner for this programme.

Customer relationships and partnership contracts

Azad’s order book exceeded Rs60 billion at the close of FY25, up roughly 90% from approximately Rs32 billion in FY24. The order book is composed almost entirely of long-term contracts ranging from five to seven years, providing multi-year revenue visibility. What follows is a contract-by-contract breakdown of every major partnership, structured by customer.

GE Vernova

GE Vernova is the largest gas turbine OEM globally, controlling approximately 34% of the global gas turbine market by installed capacity. The relationship with Azad spans multiple contract awards and a dedicated manufacturing facility.

Contract 1 (March 2024): A seven-year supply agreement valued at Rs3,115 million for gas and thermal turbine components. Azad manufactures precision airfoils and turbine components, GE Vernova integrates these into its industrial gas turbine platforms.

Contract 2 (January 2025): A six-year supply agreement valued at Rs960 million for gas and thermal turbine components, linked to the inauguration of a dedicated GE Vernova lean manufacturing facility at Azad’s Hyderabad complex on April 29, 2025. This facility is designed to GE Vernova’s global specifications and aligned with their manufacturing processes.

Contract 3 (May 2025): A six-year supply agreement valued at Rs4,525 million for steam turbine components. This contract extends Azad’s scope from gas turbine airfoils into steam turbine components, broadening the product range supplied to GE Vernova.

The three contracts together total approximately Rs8,600 million over their respective terms. The dedicated facility model means GE Vernova has invested in setting up a manufacturing line to its own specifications inside Azad’s complex, creating a physical and operational integration that makes switching suppliers costly and disruptive.

GE Vernova’s demand outlook directly drives Azad’s energy revenue. GE has approximately 80 GW of gas turbines on contract and is ramping production to 20 GW annualised by FY26. GE expects to be sold out for 2030 deliveries by the end of 2026, meaning any supplier qualified on GE platforms is looking at a multi-year demand pipeline.

Mitsubishi Heavy Industries (MHI)

MHI is the second-largest gas turbine OEM globally, controlling approximately 27% of the market. The relationship includes two major contracts and a dedicated facility.

Contract 1 (March 2025): A five-year supply agreement valued at Rs7,000 million, linked to the inauguration of a dedicated MHI lean manufacturing facility on March 12, 2025. This facility is designed to MHI’s specifications and manufactures precision airfoils and turbine components for MHI’s industrial gas turbine platforms.

Contract 2 (September 2025): An additional five-year supply agreement valued at Rs6,510 million, expanding the scope of components supplied to MHI.

The two contracts together total approximately Rs13,510 million over five years, making MHI one of Azad’s largest customers by contracted value. The dedicated facility means MHI’s processes, quality systems and logistics are embedded in the facility’s operations, creating the same switching-cost dynamics seen with the GE Vernova facility.

Japan accounted for 38% of Azad’s FY25 revenue, and MHI is the primary driver of this geographic concentration. The depth of the MHI relationship - two large contracts plus a dedicated facility - means this concentration is structural rather than transient.

Siemens Energy

Siemens Energy controls approximately 24% of the global gas turbine market. The relationship includes two contracts and a dedicated facility.

Contract 1 (July 2024): A five-year supply agreement for precision turbine components. Specific value not disclosed in available filings but forms the baseline of the relationship.

Contract 2 (January 2025): A six-year supply agreement valued at Rs8,110 million, linked to the inauguration of a dedicated Siemens Energy lean manufacturing facility on September 18, 2025. Azad manufactures precision turbine components, Siemens Energy integrates them into gas and steam turbine platforms.

The Siemens Energy dedicated facility is the third client-dedicated facility inaugurated under Phase-1, following MHI and GE Vernova. The Rs8,110 million contract is one of the largest single contracts in Azad’s portfolio by value.

Rolls-Royce

Rolls-Royce is a premier aircraft engine manufacturer, producing engines for widebody, narrowbody and business jet platforms. The relationship with Azad spans over a decade.

Contract 1 (January 2024): A long-term supply agreement structured as seven years plus a three-year extension option. Azad supplies aero engine components, Rolls-Royce integrates them into aircraft engines for platforms including widebody and potentially business jet applications.

Contract 2 (February 2025): An additional contract (terms not fully disclosed) expanding the scope of components supplied to Rolls-Royce.

The Rolls-Royce relationship is significant because it represents Azad’s deepest penetration into the aerospace engine supply chain. Rolls-Royce engines power the Airbus A350 (Trent XWB), Boeing 787 (Trent 1000) and various business jets. Being qualified as a Rolls-Royce supplier requires meeting some of the most stringent quality standards in aerospace, and the decade-long relationship indicates Azad has consistently met those standards.

Honeywell Aerospace ISC, USA

Contract (October 2024): A supply agreement valued at Rs1,424 million for APU and aerospace components. Azad supplies APU components and other aerospace parts, Honeywell integrates them into auxiliary power units and aerospace systems.

Honeywell is one of the dominant APU manufacturers globally. APUs are installed on virtually every commercial aircraft, and Honeywell’s APUs are used across Boeing and Airbus platforms. The contract gives Azad a position in the APU aftermarket, which is experiencing strong demand due to aging fleets and extended maintenance turnaround times.

Baker Hughes (Nuovo Pignone srl)

Contract 1 (March 2024): A five-year supply agreement for oil and gas drilling components. Azad supplies drill bits and other critical drilling equipment components, Baker Hughes integrates them into drilling systems.

Contract 2 (May 2025): An addition to the original contract, extending the scope for another five years. This expands the portfolio of components Azad supplies to Baker Hughes across upstream and midstream applications.

Baker Hughes controls approximately 4% of the global gas turbine market but is a major player in oil and gas equipment. The relationship gives Azad exposure to the oil and gas drilling equipment market, which is driven by exploration and production spending cycles.

Arabelle Solutions France

Contract (November 2024): A five-year supply agreement valued at Rs3,400 million for turbine components for nuclear power applications. Azad supplies precision turbine components, Arabelle integrates them into nuclear turbine systems.

Arabelle Solutions is a subsidiary of GE Vernova focused on nuclear turbine systems. The Arabelle steam turbine is the world’s largest nuclear turbine, used in nuclear power plants across France, China and other countries. This contract gives Azad exposure to the nuclear power market, which is experiencing a renaissance as countries seek zero-carbon baseload power.

India targets 22,000 MW of nuclear power capacity by 2050, and global nuclear power generation is growing approximately 2% annually during 2025-2026. The Arabelle contract positions Azad in the nuclear turbine supply chain at a time when nuclear capacity additions are accelerating.

Bharat Heavy Electrical Limited (BHEL)

Contract (January 2025): A supply agreement for precision turbine components for domestic power generation. Specific contract value not disclosed. Azad supplies precision turbine components, BHEL integrates them into Indian power plant turbines.

BHEL is India’s largest power generation equipment manufacturer. The contract represents Azad’s growing domestic revenue stream, driven by India’s push for power generation indigenisation. India’s peak electricity demand is projected to increase from 241 GW in 2024 to 366 GW by 2031, creating sustained demand for domestic turbine manufacturing.

GTRE (DRDO, Ministry of Defence)

Contract (May 2024): A single-source Industry Partner contract for end-to-end manufacturing, assembly and integration of a completely assembled Advanced Turbo Gas Generator Engine. Azad is the sole authorised manufacturer for this engine programme.

The contract structure is fundamentally different from Azad’s other partnerships. In every other contract, Azad manufactures components that the OEM integrates into a larger system. In the GTRE contract, Azad is responsible for the complete engine - manufacturing, assembly and integration. This elevates Azad from a Tier 3 component supplier to a Tier 1 system integrator for this specific programme.

Near-term revenue is limited at Rs50-150 million, but the long-term optionality is Rs300-1,000 million or more, contingent upon indigenous engine serialisation. The contract also provides defence aero-engine qualification experience that could open doors to additional defence propulsion programmes.

Azad VTC (strategic acquisition)

Azad acquired Azad VTC as a small strategic acquisition to strengthen vertical integration and execution capability. The acquisition is targeted at adding specific process capabilities rather than scaling revenue inorganically. Details on the acquisition structure and specific capabilities added have not been extensively disclosed, but the transaction fits the pattern of capability-driven investments that characterise Azad’s growth strategy.

Contract structure summary

The common elements across Azad’s major contracts are:

Fixed-price with pass-through: Most contracts follow fixed-price structures with a raw material volatility absorption threshold of approximately 4-5%. Beyond this threshold, costs are passed through to the OEM, preserving margin stability.

Multi-year tenures: Contracts range from five to seven years (plus extension options), providing revenue visibility.

Customer-approved raw materials: Raw material sourcing is restricted to customer-approved sources, meaning Azad cannot substitute materials without OEM approval. This contributes to supplier concentration on the raw material side.

Dedicated facilities: Three major customers (GE Vernova, MHI, Siemens Energy) have dedicated manufacturing facilities within Azad’s Hyderabad complex, deepening operational integration.

Competitive landscape

Structure of the precision turbine component industry

The global market for precision-machined turbine airfoils, blades and hot gas path components is served by two categories of manufacturers. The first category comprises large, vertically integrated OEMs or their captive subsidiaries - companies like Howmet Aerospace, PCC Airfoils (Berkshire Hathaway) and IHI Corporation - that have their own casting operations, forge shops and coating facilities. These companies control the upstream supply chain from alloy production through to finished component. The second category comprises independent, specialist precision machining houses that buy raw material (forgings, castings or bar stock) from approved sources and machine them to OEM specifications. Azad sits in this second category.

Within the independent specialist category, there are six companies globally that compete directly with Azad’s business model. These are build-to-print suppliers serving the same OEM customers with similar products. The competitive dynamics differ by segment.

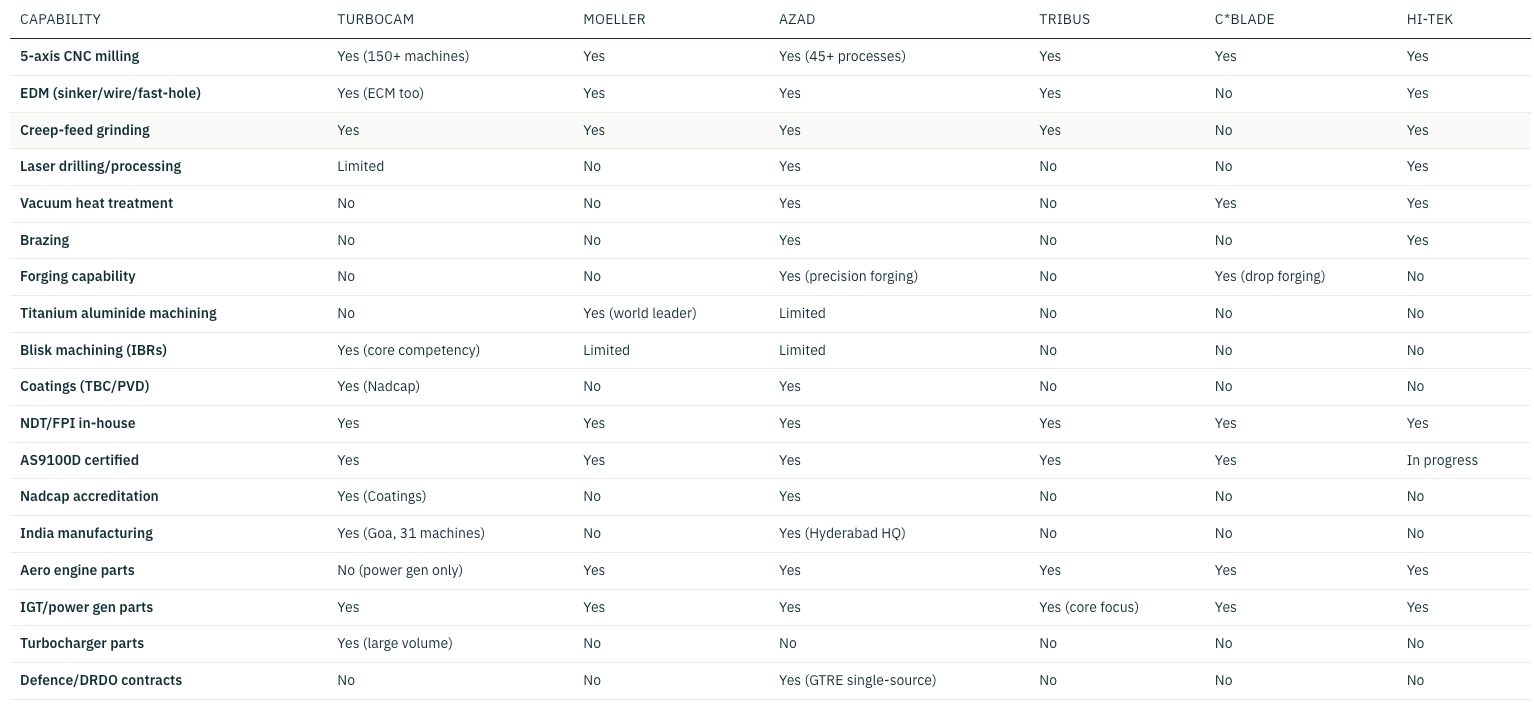

Tier A peers: the six direct competitors

The following table maps the six companies that operate as independent, specialist precision machine manufacturers for turbine airfoils, blades, vanes and hot gas path components.

The revenue-per-employee metric reveals Azad’s structural cost advantage. At $43K revenue per employee, Azad generates less revenue per person than every peer except C*Blade’s lower bound. But this reflects India’s wage structure, not inefficiency. Azad’s labour costs are approximately 70% lower than US-based peers and 30-40% lower than China-based peers. The lower revenue per employee is offset by proportionally lower costs, producing margins that already exceed those of much larger peers.

TURBOCAM International - the primary benchmark

TURBOCAM is Azad’s single most important competitive benchmark. Both companies are precision 5-axis machining houses serving the same OEMs with similar products. TURBOCAM has 2.4x Azad’s revenue but a fundamentally different cost structure: $158K revenue per employee (US and EU wages) versus Azad’s $43K (India wages).

TURBOCAM operates 150+ 5-axis machines across four countries (US, India, UK, Romania). Its India operation in Goa has 31 machines, approximately 120 employees and generates approximately $6 million in revenue. This Goa facility is small relative to Azad’s Hyderabad complex and represents a fraction of TURBOCAM’s global capacity.

The competitive risk from TURBOCAM is specific: its Goa facility could be scaled up to compete directly for India-cost-advantage work. TURBOCAM has demonstrated it can win dedicated production contracts on next-gen programmes, including a Pratt and Whitney GTF vane plant. However, TURBOCAM’s focus is broader than Azad’s - turbochargers are a large revenue share for the company, and this dilutes its competitive intensity in the energy airfoil niche where Azad operates.

A critical structural difference is access to capital. TURBOCAM is private and family-owned, limiting its ability to raise growth capital. Azad’s public listing on the NSE and BSE gives it a structural fundraising advantage, as demonstrated by the approximately Rs7 billion QIP that funded the Phase-1 expansion.

Capability comparison across Tier A peers

The following matrix compares technical capabilities across the six Tier A peers. A checkmark indicates confirmed capability, a cross indicates no evidence of capability.

Azad has the broadest capability set among Tier A peers, spanning forging, 5-axis machining, EDM, laser, heat treatment, brazing and coatings, all performed in-house. TURBOCAM leads in blisk and IBR machining and ECM. Moeller is the undisputed leader in titanium aluminide machining. Only Azad and TURBOCAM have India manufacturing operations. Only Azad has active defence and DRDO production contracts.

Howmet Aerospace - the closest global peer

Howmet Aerospace is the closest global peer to Azad Engineering by business model. Both companies manufacture high-precision rotating components - blades, vanes, housings and airfoils - for aero engines and industrial gas turbines. Both supply the same OEM customers: GE, Siemens, Honeywell, Rolls-Royce and Mitsubishi. Both derive their competitive moat from multi-year OEM qualification cycles that create near-impenetrable entry barriers.

Howmet’s trajectory over 2020-2025 provides a credible template for Azad’s own journey. Howmet grew revenue from $4.3 billion to $8.3 billion, expanded EBITDA margin from 22% to 29%, saw its PE re-rate from 23x to 65x, and delivered approximately 400% stock returns over that period. Howmet now generates over $1.4 billion in annual free cash flow at 93% net income conversion.

The key structural difference is cost base. Azad’s margins already exceed Howmet’s levels - a function of India’s labour and power cost advantage. Howmet operates from the US, UK, France and Czech Republic with a global manufacturing footprint. Azad operates from a single Hyderabad complex with approximately 80% of revenue from exports.

Howmet is approximately 180x larger than Azad by revenue, but Azad is growing 2.7x faster. Howmet’s revenue grew at approximately 13% over FY21-25, while Azad grew at approximately 39% over the same period. Both operate in the same secular demand upcycle - global aero engine demand plus industrial gas turbines - meaning Azad’s trajectory is structurally validated by what its global peer is experiencing.

Other global competitors

Beyond the Tier A precision machining specialists, Azad competes with several larger, more integrated players that participate in overlapping product categories.

PCC Airfoils / Berkshire Hathaway Precision Castparts (US): Approximately $2.5 billion in estimated revenue from the airfoil segment. Berkshire Hathaway owned. Number one in structural castings and investment castings, present on every jet engine programme. The advantage over Azad is scale and vertical integration from alloy through to coating. The disadvantage is cost structure - US-based manufacturing with US labour costs.

Chromalloy (US): Approximately $800 million to $1 billion in estimated revenue. Veritas Capital owned. Strong in MRO and aftermarket. Advanced Airfoil Components was sold to Siemens in 2022. Chromalloy’s strength is in repair and overhaul rather than new part manufacturing, which is a different segment of the value chain from Azad’s build-to-print model.

Doncasters Group (UK): Approximately $500-700 million in estimated revenue. Dubai International Capital owned. Acquired Uni-Westinghouse Pol in 2022 for superalloy castings. Turbine airfoils, compressor airfoils, rings and casings. Competes directly with Azad in the energy turbine segment but from a European cost base.

Consolidated Precision Products (US): Approximately $400-600 million in estimated revenue. Warburg Pincus backed. Strong in structural and airfoil castings. Investment castings for aero and IGT. Acquired Selmet Inc. to expand capabilities.

Hitchiner Manufacturing (US): Approximately $300-400 million in estimated revenue. Pioneer in counter-gravity casting. Strong in smaller complex airfoils. Competes in the casting segment rather than the machining segment.

IHI Corporation (Japan): Approximately $2 billion in the aero engine segment. Pratt and Whitney RRSP (Revenue Share Partner) on the PW1100G. Makes full low-pressure turbine modules. IHI is a more integrated player than Azad, manufacturing complete modules rather than individual components.

Impro Precision Industries (HK/China): Approximately $250-350 million in estimated revenue. Listed in Hong Kong. Expanding aerospace share. Competitive on cost. Impro is the closest competitor to Azad from a cost-structure perspective, operating from China with similar labour cost advantages.

Indian competitors

PTC Industries / Aerolloy (India): Approximately Rs7 billion FY25E revenue. First Indian company to achieve single-crystal casting capability. LEAP engine supplier to Safran. Acquired Trac Precision (UK) for post-cast machining capabilities. PTC is building a different capability set from Azad - it is focused on casting (investment casting, SC/DS castings, titanium castings) while Azad is focused on machining. They could potentially be complementary rather than directly competitive, but both are positioning themselves as comprehensive turbine component suppliers.

Godrej Aerospace (India): Approximately Rs4-5 billion in estimated revenue. Delivered the first serial KDE engine. Kaveri turbine blade maker. ISRO liquid engine sole fabricator. Godrej has deeper defence engine experience than Azad, having manufactured components for the Kaveri engine programme. The company also has a relationship with ISRO as the sole fabricator of liquid engines, giving it space propulsion credentials.

Bharat Forge (India): Approximately Rs18 billion in the aerospace business unit. NADCAP certified. Developing ab-initio gas turbine engines (40-400 kgf thrust class). Acquired Zorya Mashproekt (Ukraine) for marine gas turbine capabilities. Bharat Forge is the largest Indian competitor by revenue and is pursuing a more ambitious strategy of developing complete gas turbine engines rather than just components. The Zorya acquisition gives it marine turbine technology that Azad does not possess.

Where Azad wins and where it faces pressure

Azad wins on three dimensions against the Tier A peer set. First, cost structure: at $43K revenue per employee versus $158K for TURBOCAM and $365K for Moeller, Azad’s India cost base provides a structural margin advantage of approximately 30% over global peers. Second, capability breadth: Azad has the broadest in-house process set among Tier A peers, spanning forging through coatings. Third, capital access: as a public company on the NSE and BSE, Azad can raise growth capital through equity issuance, something private peers like TURBOCAM and Hi-Tek cannot do easily.

Azad faces pressure on two dimensions. First, scale: at approximately $65 million in revenue, Azad is roughly 2.4x smaller than TURBOCAM and 180x smaller than Howmet. This means Azad has less bargaining power with raw material suppliers and less ability to absorb large programme ramps. Second, the TURBOCAM Goa facility represents a direct competitive threat in the India-cost-advantage segment, though TURBOCAM’s broader focus on turbochargers dilutes its competitive intensity in energy airfoils.

Against larger integrated players like Howmet and PCC, Azad does not compete head-to-head on casting-intensive programmes. Howmet and PCC control the single-crystal and directionally-solidified casting processes that Azad does not perform. Azad’s niche is precision machining of forged or cast blanks into finished airfoils and components, which is a different step in the value chain. The competitive dynamic is more complementary than substitutive - Howmet may supply castings that Azad then machines, or they may compete for machining-only programmes where the casting is sourced from a third party.

Industry context and demand drivers

Aerospace and defence industry

The global aerospace sector was valued at $402.75 billion in 2025 and is expected to reach $791.78 billion by 2034. Commercial aerospace accounts for approximately $230 billion of this, growing at roughly 5% annually. The growth is driven by post-COVID recovery in air travel, rising disposable incomes in emerging markets, and global connectivity expansion.

The most important structural feature of the aerospace industry today is the unprecedented gap between demand and supply. Global aircraft backlog stands at over 17,000 aircraft - equivalent to more than 12 years of production at current rates. In 2024, Airbus delivered 766 aircraft (down from a 2019 high of 863) and Boeing delivered just 348 (down from 806 in 2018). Aircraft delivered in 2024 took 6.8 years to make it to airlines, up from 4.5 years in 2018.

This backlog is not a temporary phenomenon. It is driven by multiple structural factors: persistent skilled labour shortages in western manufacturing economies, supply chain disruptions from COVID and geopolitical conflicts, extended certification timelines (Boeing 737 MAX 7/10 and 777X are in their fourth and fifth years of certification respectively), and increased maintenance turnaround times that keep older aircraft in service longer.

The aging fleet creates a parallel demand driver. The average aircraft age climbed to 13.4 years in 2024 from 12.5 years in 2023. Average annual flight hours rose approximately 15% to roughly 2,800 hours in 2024 from approximately 2,400 hours in 2022. Older aircraft flying more hours means higher maintenance intensity, more frequent component replacement and stronger aftermarket demand. Global MRO spend is projected to reach $156 billion by the end of the forecast period, up 31% from 2025, growing at 2.7% annually over 2025-2035.

The incremental costs imposed on airlines by these supply chain constraints are substantial: approximately $4.2 billion in fuel inefficiency from operating older aircraft, $3.1 billion in additional maintenance costs, $2.6 billion in excess engine leasing costs, and $1.4 billion in inventory holding costs. These costs create powerful incentives for airlines and OEMs to accelerate supply chain diversification.

Why global OEMs are coming to India

Four structural factors are driving aerospace OEMs to source from India:

First, the unprecedented aircraft backlog of approximately 14 years means OEMs cannot meet demand from existing supply chains. They need new qualified suppliers, and they need them quickly.

Second, post-COVID supply chain re-orientation has pushed OEMs to diversify and regionalise supply chains, reducing dependence on single-country sourcing. India offers a stable, scalable and increasingly qualified alternative.

Third, India provides a structural cost advantage with labour costs approximately 70% lower than the US and 30-40% lower than China, while maintaining improving quality standards. This allows OEMs to lower production costs without compromising precision or reliability.

Fourth, India has a large and growing base of STEM-trained engineers and technicians, supported by engineering institutes and vocational programmes. This talent availability supports long-term scaling of complex, knowledge-intensive aerospace work.

India’s domestic aviation market reinforces this. Domestic passenger volume reached 161.3 million in CY24, and IATA projects annual traffic will triple to 425 million by 2044. India’s fleet has more than doubled in the past decade to approximately 890 aircraft, with 2,325 on order - one of the largest order books globally. Fifty new regional airports are planned in the next five years. This creates a domestic demand pull that complements the export-driven manufacturing opportunity.

Energy industry

The energy equipment sector is entering a structural, multi-decade upcycle driven by electricity demand, grid stress and baseload reliability needs. Global gas turbine installations reached approximately 70.8 GW and 964 units in 2025.

The global gas turbine market is highly concentrated. GE Vernova controls 34%, Mitsubishi Power 27%, Siemens Energy 24%, Baker Hughes 4% and others 11%. This concentration benefits suppliers like Azad because it means a small number of OEMs control the majority of turbine orders, and qualifying with these OEMs gives access to a large share of the market.

Electricity demand is rising at approximately 3% annually, versus earlier projections of 2-2.5%, driven by AI data centres, re-industrialisation and electrification of transport, buildings and industry. This is not a cyclical spike but a structural shift that sets up a longer and larger capex cycle.

Gas turbines are positioned as the “bridge baseload” of the energy transition. Despite high renewable energy penetration, gas turbines are indispensable due to grid instability at high RE penetration, the need for fast-ramping reliable baseload for data centres, and delays in transmission, permitting and fuel availability. GE has approximately 80 GW of gas turbines on contract and is ramping to 20 GW annualised by FY26. GE expects to be sold out for 2030 deliveries by the end of 2026.

Two-thirds of gas-fired capacity under construction is in Asia, led by China with 151 GW in development and 46 GW under construction. Nearly 47% of turbines under construction (82 GW) are hydrogen-ready, reflecting a shift toward cleaner fuels. This means the turbines being built today will still be operating - and requiring replacement components - for decades.

India’s peak electricity demand is projected to increase from 241 GW in 2024 to 366 GW by 2031, driving investments in domestic power generation infrastructure. This supports demand for components supplied to BHEL for domestic turbine manufacturing.

Nuclear power

Global nuclear power generation is growing approximately 2% annually during 2025-2026, supported by reactor restarts in Japan, new builds in China and India, and steady output from the US and France. India targets 22,000 MW of nuclear capacity by 2050, with multiple new reactors under construction and collaborations with Russia, France and the US. The Arabelle Solutions contract gives Azad exposure to this nuclear turbine supply chain.

Steam turbine market

The global steam turbine market was valued at $17-19 billion in 2024 and is expected to grow at approximately 2.5% annually to reach $21-23 billion by 2030-2034. The steam turbine services and MRO market is larger, at $19.5 billion in 2024 and expected to reach $31.8 billion by 2034 at 5% annually. The GE Vernova steam turbine contract (Rs4,525 million, six years) gives Azad direct exposure to this segment.

Oil and gas industry

The oil and gas industry is experiencing a cyclical recovery driven by strong energy demand, geopolitical energy security concerns and renewed investment in hydrocarbon infrastructure. While long-term energy transition policies promote renewables, oil and natural gas remain critical to the global energy mix, particularly for transportation, petrochemicals and baseload power generation.

Natural gas is increasingly positioned as a transition fuel, driving investments in gas infrastructure including LNG liquefaction plants, regasification terminals, pipelines and gas turbine-based power generation. Energy security concerns following geopolitical disruptions have prompted countries to diversify supply chains and increase domestic hydrocarbon production, driving higher spending on oilfield equipment and drilling components.

The oil and gas equipment supply chain is characterised by high entry barriers due to stringent qualification requirements, long certification cycles and the need for advanced manufacturing capabilities. The global supplier base for critical components remains highly concentrated, which benefits established suppliers like Azad who are already qualified with major OEMs like Baker Hughes.

India’s position in the global supply chain

India provides a structural cost advantage with labour costs approximately 70% lower than the US and 30-40% lower than China, while maintaining improving quality standards. This is the fundamental driver of OEM supply chain diversification to India.

The structural shortage of skilled labour in aerospace globally further reinforces India’s advantage. In 2023, a reported 40% of FAA certification engineers had less than two years of experience. The aging aerospace workforce in the US and Europe, combined with limited inflow of younger technically trained workers, has created persistent shortages of highly skilled roles. India’s STEM talent pool addresses this gap from a different geography.

India’s aerospace exports touched $6.9 billion in 2025, reflecting the growing integration of Indian manufacturers into global aerospace supply chains. New MRO hubs are being set up by companies like Safran in Hyderabad, Boeing in Nagpur and an Air India-Pratt and Whitney JV in Mumbai, further deepening the aerospace ecosystem.

Growth triggers

Phase-1 capacity expansion completion

The Phase-1 expansion, funded through the approximately Rs7 billion QIP, comprises nine new and planned client-dedicated lean manufacturing facilities. Three have been inaugurated (MHI in March 2025, GE Vernova in April 2025, Siemens Energy in September 2025). The expansion raises total potential revenue capacity from approximately Rs4.5 billion to approximately Rs20 billion - a roughly 10x increase in revenue visibility. Projected revenue with existing capex plans reaches approximately Rs22.5 billion.

The timeline for full commissioning is FY26-FY27. Each facility is estimated to support approximately Rs2 billion in revenue at maturity. The dedicated facility model means revenue ramp depends on facility commissioning, equipment installation, OEM qualification of the new facility and production ramp-up - a process that typically takes 12-18 months per facility from inauguration to meaningful revenue contribution.

Rising aerospace and defence revenue mix

The aerospace and defence segment grew 84.1% in FY25 to Rs807 million, reaching 17.9% of total revenue. This growth was driven by completed qualification cycles and execution strength across Boeing 737, Airbus A320/A350 and Gulfstream G550 platforms.

Management targets approximately 50% aerospace and defence revenue mix over the medium term. Achieving this would require the segment to grow at a significantly faster rate than the energy segment, which means continued qualification wins on new platforms and engine variants. The segment’s growth trajectory is supported by the record global aircraft backlog, the MRO super cycle and OEM supply chain diversification to India.

Expansion into combustion components

Azad is moving up the turbine value chain from compressor airfoils into combustion components. Combustion components represent a more complex and higher-value part of the turbine, requiring higher heat tolerance materials and more sophisticated manufacturing processes.

This expansion increases wallet share per turbine platform. If Azad supplies only compressor airfoils to an OEM, it captures a fraction of the total component spend per turbine. By adding combustion components, Azad can multiply its revenue per turbine platform from the same customer without needing to win a new customer. The OEM already knows Azad’s quality systems and has integrated it into their supply chain, making it easier to add new part families to an existing qualified supplier than to qualify a new one.

GTRE advanced turbo gas generator engine

First deliveries of fully integrated turbo engines are expected by early 2026. While near-term revenue is limited (Rs50-150 million), the long-term optionality is significant (Rs300-1,000 million or more) if indigenous engine serialisation proceeds. The contract also provides defence aero-engine qualification experience that could open doors to additional defence propulsion programmes.

Global electricity demand surge

Electricity demand is rising at approximately 3% annually versus earlier projections of 2-2.5%, driven by AI data centres, re-industrialisation and electrification. This supports OEM order flows for GE Vernova, Mitsubishi and Siemens Energy, which in turn drives demand for Azad’s precision components. GE’s expectation of being sold out for 2030 deliveries by the end of 2026 illustrates the demand pipeline.

OEM supply chain diversification to India

The combination of an unprecedented aircraft backlog (approximately 14 years), post-COVID supply chain re-orientation, India’s structural cost advantage and deep STEM talent pool is driving OEMs to source from India. Azad is a qualified, NADCAP-accredited, AS9100D-certified supplier with a decade-plus track record with major OEMs, positioning it as a primary beneficiary of this trend.

Wallet share expansion

Azad’s FY25 revenue of approximately USD 65 million represents less than 0.5% of the global aircraft engine blade market. Even within the narrower precision-machined airfoil niche estimated at USD 3-4 billion globally, Azad’s share is only 1.5-2%. Expanding this share to 3-4% - still a small fraction of the total market - would represent a meaningful step-up in revenue.

Phase-2 capacity expansion

Beyond Phase-1, Azad has announced plans for a Phase-2 capacity expansion to support execution of the growing order pipeline and further enhance OEM integration. Specific details on capacity, timeline and investment have not been disclosed, but the company has indicated that Phase-1 facilities alone may not be sufficient to meet demand from existing and prospective customers.

Nuclear and advanced turbine programmes

Participation in nuclear and advanced turbine programmes adds long-term growth optionality and a diversified revenue stream. The Arabelle Solutions contract (Rs3,400 million, five years) gives Azad exposure to nuclear turbine systems. India’s target of 22,000 MW of nuclear capacity by 2050, combined with global nuclear power growth of approximately 2% annually, creates a multi-decade demand pipeline for nuclear turbine components.

Key risks

Promoter and key person risk